Research and Development or Film Relief and tax credits

This screen is accessed via the Data input tab within the tax return. Use this section to claim Research & Development relief, Film Relief or R&D/Film Tax Credits. Only companies which are based in the UK, and that pay Corporation Tax, are eligible to apply for Research and Development (R&D) Tax Credits. There are two schemes for R&D tax relief. One is for SMEs and the other is for Large Companies, both are available within Taxfiler.

This section has three tabs:

- Enhanced expenditure (includes Film Tax Credit)

- R & D Tax Credit

- Above The Line R&D Tax Credit (RDEC)

For further explanation on claiming Research and Development Expenditure Credit read the following article: https://www.taxadvisermagazine.com/article/taking-credit

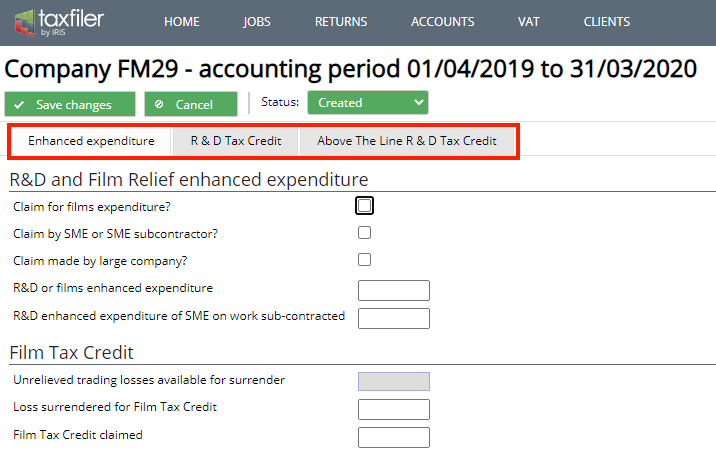

Enhanced expenditure

This tab of the R&D or Film Relief and tax credits section allows input of enhanced expenditure totals and Film Tax Credit. Theatre tax relief can be entered as Film tax relief in Taxfiler.

R&D and film relief enhanced expenditure

- Claim for films expenditure? – tick the box if claiming films expenditure.

- Claim by SME or SME subcontractor? – tick the box if the claim is made by an SME or SME subcontractor.

- Claim made by large company? – tick the box if the claim is made by a large company.

- R&D or films enhanced expenditure – enter the R&D or films enhanced expenditure.

- R&D enhanced expenditure of SME on work sub-contracted – enter the enhanced expenditure of an SME on work that is sub-contracted from a large company.

Film tax credit

- Unrelieved trading losses available for surrender – this field shows the current value of unrelieved trading losses, brought through from the Trade Summary tab

- Loss surrendered for Film Tax Credit – enter the amount of the loss that is to be surrendered for Film Tax Credit.

- Film Tax Credit claimed – enter the amount of tax credit claimed.

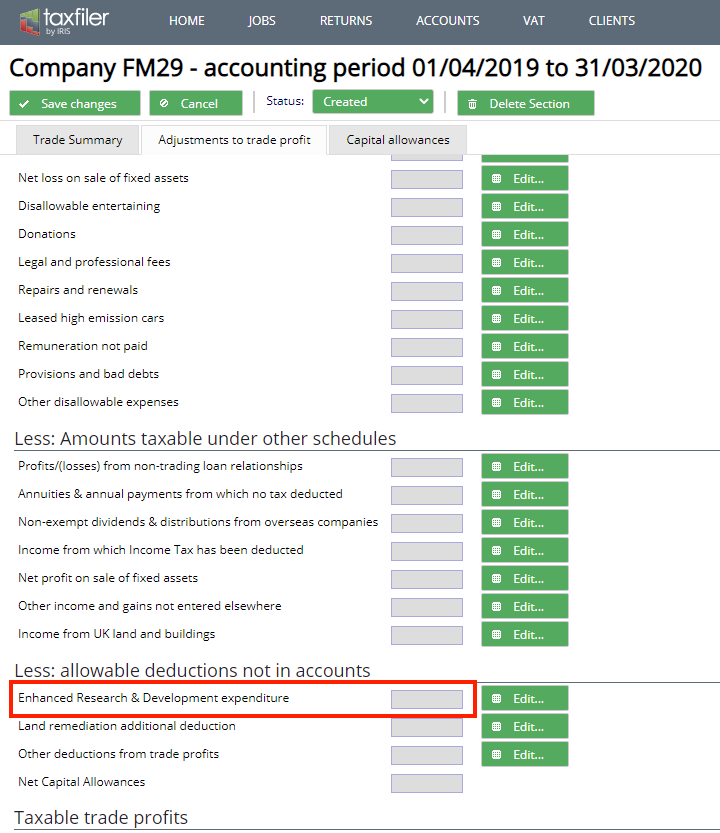

Enhanced expenditure must also be entered on the adjustments to trade profit in the trading profits section from the data input tab in the tax return.

R & D Tax Credit

This tab of the R&D or Film Relief and tax credits section allows calculation of the R&D Tax Credit.

Research and Development Tax Credit

- Surrender trade losses for R&D Tax Credit? – tick the box to surrender trade losses for an R&D Tax Credit.

- Enhanced expenditure from trade (A) – this field shows the enhanced R&D expenditure as entered in the trading profits screen.

- Unrelieved trade losses for period (B) – this field shows the unrelieved trading losses for the period from the trading profits screen.

- Surrenderable loss (lower of A and B) – this field shows the surrenderable loss.

- Rate – enter the rate at which the tax credit is surrendered. This rate can be edited as required.

- R&D tax credit – this field shows the calculated R & D tax credit.

Override calculated tax credit

It is possible to override the calculated tax credit, in which case the computation will not show the calculation derived from the section above. You will need to attach a computation of the tax credit to the Tax Return.

- Override calculated tax credit? – tick the box to override the calculated tax credit.

- Losses surrendered for R&D tax credit – enter the losses surrendered.

- R&D tax credit – enter the R&D tax credit that is claimed.

Above The Line R&D Tax Credit (RDEC)

This page provides calculation of the Research and Development Expenditure Credit (RDEC), also known as Above The Line Tax Credit.

RDEC and the current large company scheme co-exist until 31 March 2016, after which time the existing large company scheme will only continue for expenditure incurred prior to that date until such expenditure is treated as deductible in a CT computation. Once a company has claimed RDEC for the first time, it has effectively elected into RDEC and the election is irrevocable.

SMEs will be able to claim the RDEC in the same circumstances as they can currently claim under the existing large company scheme. As with loss making large companies SMEs will now be able to claim a payable credit under the RDEC subject to certain restrictions and set offs on such claims.

Ensure you tick the box ‘Claim Above The Line Research & Development Expenditure credit’, this will open additional fields which need to be completed. Enter the value for PAYE and Class 1 NIC liabilities for the period as this determines the cap on the claim.

Above The Line R7D expenditure credit

- Claim Above The Line Research & Development Expenditure Credit? – tick the box to indicate a claim for credit under the RDEC scheme.

- Qualifying expenditure – enter the qualifying expenditure for the period.

- Rate – select the rate from the drop-down list, that applies to the expenditure, this is 12% for large companies and 49% for ring-fenced trades.

- Calculated tax credit – Taxfiler will display the maximum calculated tax credit for period.

- Tax credit b/fwd and/or surrendered from group – enter any brought forward tax credit or tax credit surrendered from other group companies.

- Research and Development tax credit (Box 530) – Taxfiler displays the total tax credit, including brought forward and surrendered tax credits.

- Amount to offset against Corporation Tax for this period – enter the amount of credit to set off against Corporation Tax due in this period.

- Amount remaining after set-off – Taxfiler displays the amount remaining after set-off.

- Calculated credit less CT at main rate – Taxfiler will calculate the net R&D tax credit as reduced by the amount of Corporation Tax payable at the relevant rate.

- Lower of amount remaining and net expenditure credit – Taxfiler will show the lower of the tax credit remaining after set-off and the calculated credit reduced by CT.

- PAYE and Class 1 NIC liabilities for the period – the credit that can be claimed in a period is capped by the PAYE/NIC of the R&D staff (with no restriction for time spent on qualifying R&D activity) and externally provided workers provided by the same group as the claimant (restricted to the proportion of time spent on qualifying R&D activity). Enter the total amount of applicable PAYE and Class 1 NIC for relevant workers.

- Expenditure credit carried forward to next period – Taxfiler displays the amount which exceeds the cap. This should be carried forward and treated as an expenditure credit for the next accounting period.

- Amount available for set-off – Taxfiler displays the net amount of capped RDEC available for set-off.

- Amount to set against Corporation Tax for other periods – enter the amount required to be set off against Corporation Tax for other periods.

- Amount surrendered to group – enter the amount to be surrendered to other group companies.

- Amount set off against other company liabilities – enter the amount required to set-off against other company liabilities to HMRC.

- Payable Research & Development Tax Credit – Taxfiler displays the final payable tax credit.