Research and Development or Creative Industry relief and tax credits

This screen is accessed via the data input tab within the tax return. Use this section to claim Research & Development relief, Creative industry reliefs or R&D/Creative industry tax Credits. Only companies which are based in the UK, and that pay Corporation Tax, are eligible to apply for Research and Development (R&D) Tax Credits. There are two schemes for R&D tax relief,

- Claims to an enhanced deduction available to SMEs only and

- Research & Development expenditure credit (Above The Line). This is available to both SME’s on certain expenditure and for large companies.

This section has three tabs:

(Click the links above for specific help on Research & Development tax credits.)

CT600L (2022) Version 3 – HMRC Validations

There are several HMRC validations that are incorrect maybe encountered when attempting to submit a CT600L to HMRC. Online filing pre validations will be shown where these HMRC validations arise. Some validations will mean that the CT600 cannot be filed online, and a paper return will have to be sent to HMRC. See HMRC’s ‘Changes and issues affecting the Corporation Tax online service page for more information. HMRC will correct these validations in a later update to the online service. To summarise it is not possible to file CT600L online in the following where:

- For return periods starting before 1/4/2022

- Box L65 – where there is a Step 2 notional tax charge to carry forward or a value of income tax deducted from profits (box 515 on CT600)

- CT600 Box 660 – this box should not be completed if a claim to an SME Research & Development tax credit is not being made for periods starting on or after 1/4/2022.

There are two remaining incorrect validations that will not prevent a successful submission of the CT600L because these have been accommodated by altering the population of the form.

- Box L167/L167A – these boxes have been completed although not relevant for these earlier periods to allow the return to be filed online. This applies where a claim is being made for SME R & D tax credit and/or SME Research & Development expenditure credit.

- Box L150 – the value in box L150 includes box L129 twice. L140 already includes box L129.

Changes to CT600 – Boxes 530, 570, 605

HMRC have made changes to the population of Research & Development tax credits boxes in the Tax reconciliation section on page 6 of the CT600 (2021) Version 3 that differs from previous versions of the tax return.

- Box 530 – the amount of Research & Development credit no longer includes the full amount of the payable credits but is now:

- Research & Development tax credit set off against other liabilities arising in the Return period such as tax on Loans to Participators

- Research & Development Expenditure Credit used to discharge the Corporation Tax liability and amounts set off against other liabilities arising in the Return period such as tax on Loans to Participators

- Box 570 – As a result of the limit to the values now being shown in box 530, box 570 will no longer show payable Research & Development credits.

- Box 605 – as a direct result of the changes to the previous boxes any overpayment arising from the claim to a payable tax credit will no longer appear in this box. The payable tax credits continue to be shown in boxes 875 and 885.

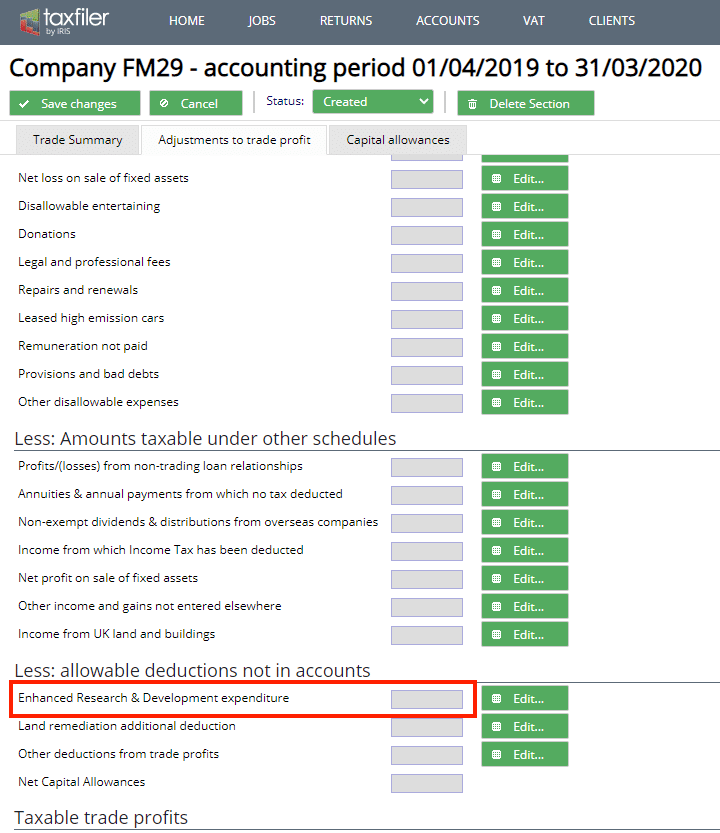

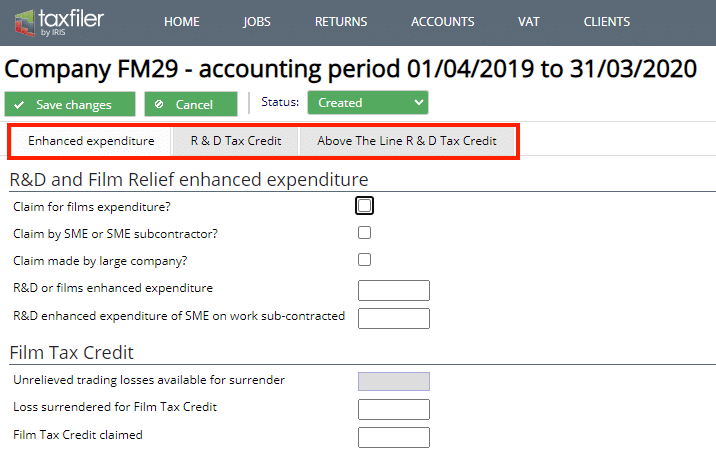

Enhanced expenditure

This tab of the R&D or Creative Industry Relief and tax credits section allows input of enhanced expenditure totals and Creative Industry Tax Credit.

R&D and Creative Industry Relief enhanced expenditure

- ‘Claim by SME or SME subcontractor?’ Tick the box if the claim is made by an SME or SME subcontractor.

- ‘Claim made by large company?‘ Tick the box if the claim is made by a large company.

- ‘R&D enhanced expenditure‘ Enter the R&D enhanced expenditure. Due to an incorrect HMRC validation do not complete this box if not claiming an SME Research and Development Tax credit.

- ‘Creative industries enhanced expenditure’ Enter the amount of enhanced Creative industry enhanced expenditure

- ‘R&D enhanced expenditure of SME on work sub-contracted‘ Enter the enhanced expenditure of an SME on work that is sub-contracted from a large company.

Creative Industry Tax Credit

Note: The following list of creative industry tax credits is only available for accounting periods ending in 2021. Earlier periods will not see this option.

‘Creative Industry type’ Select the relevant creative industry tax credit being claimed from the list:

- Animation

- Children’s Television

- High-end Television

- Museum & Galleries (Non-Touring)

- Museum & Galleries (Touring)

- Orchestra

- Theatre (Non-Touring)

- Theatre (Touring)

- Video games

- ‘Unrelieved trading losses available for surrender‘ This field shows the current value of unrelieved trading losses, brought through from the Trade Summary tab

- ‘Loss surrendered for Creative Industry Tax Credit’ Enter the amount of the loss that is to be surrendered for Creative Industry Tax Credit.

- ‘Creative Industry Tax Credit claimed‘ Enter the amount of tax credit claimed.

Enhanced expenditure must also be entered on the adjustments to trade profit in the trading profits section from the data input tab in the tax return.