Carried back losses CT600

The following help pages show the process for carrying back a loss to a prior profit-making year for a CT600 return, this is different for a SA100 return (see losses carried back for SA100)

In the current loss-making year,

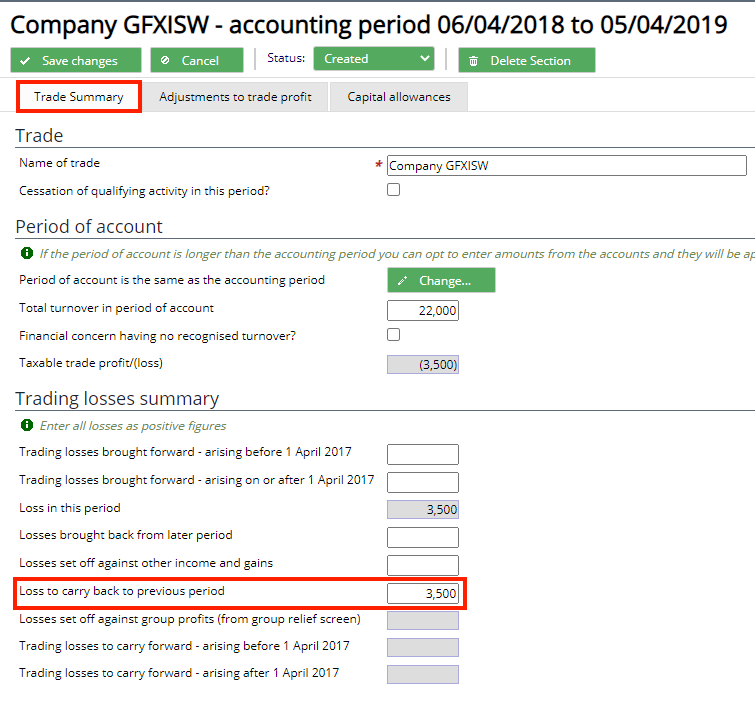

- Enter the loss to carry back to previous period on the Trade Summary screen, this is accessed via the data input tab, Trading Profits, within the tax return.

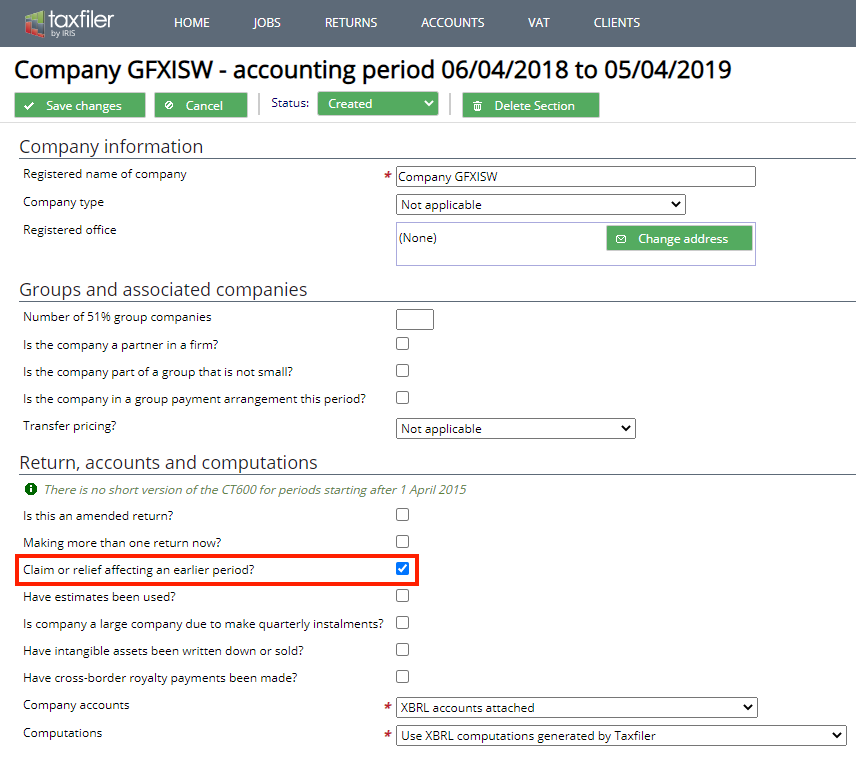

- Tick the box for ‘Claim or relief affecting an earlier period?’ in the Company information screen, this is accessed via the data input tab within the tax return and click on save changes.

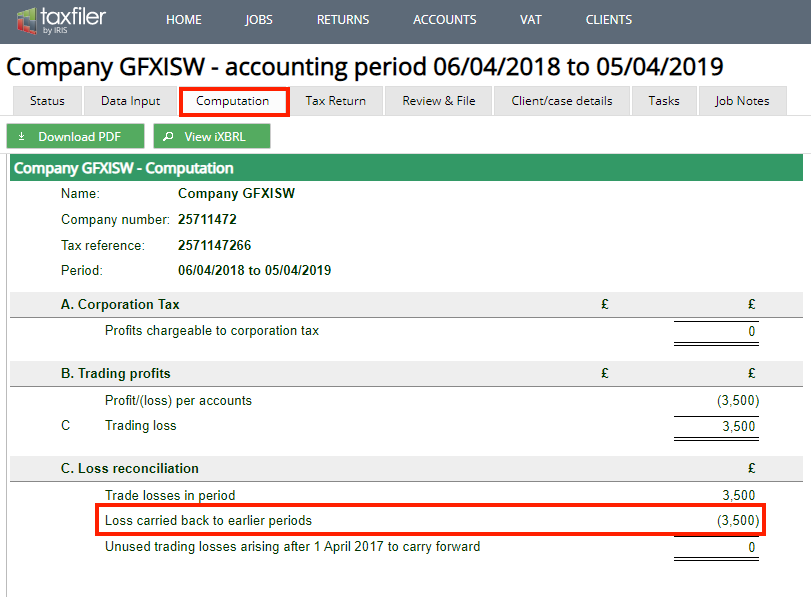

- The computation will now reflect that the loss is being carried back to an earlier period

You can submit this return to HMRC.

If you are still within the amendment window to submit an amended return, this can be done via Taxfiler. If the amendment window has passed, you will need to do this manually. If you need to carry the loss back to multiple periods, you will need to submit amended returns for each affected year separately

Submitting the amended return via Taxfiler:

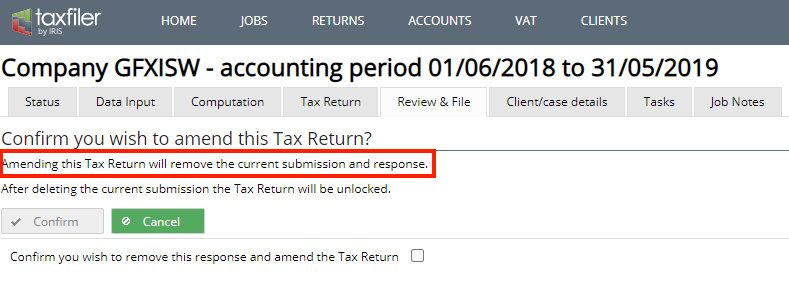

You will need to ‘Unlock’ the prior year return, please make sure that you have a copy of the receipt for the original return, as this will be removed from Taxfiler when you unlock the return. This is accessed via the ‘Review & File’ tab

Confirm that you wish to remove this response and amend the tax return.

Enter the amount of the loss being carried back onto the Trading Summary screen, this is accessed via the data input tab, Trading profits screen within the tax return.

Submit the amended return for the earlier year with an updated computation. Should you not wish to submit the previous year return online you will need to submit it manually.

Submitting the amended return manually

Attach a note to the current year explaining how the loss is being used and showing how the repayment is computed. Alternatively attach a PDF of the earlier year computation showing the amended figure and detailing the repayment.

It is recommended that if attaching a PDF version of the prior year/(s) to the current year return, to write a letter to HMRC setting out the details of the loss claim and requesting the repayment. This is sometimes more likely to be actioned in a timely manner than when relying on the processing of the current year form.

Summary of the steps:

- Go to the Trading profit screen in the later loss making period

- Enter the loss in the Loss to carry back to previous period in the Trading losses summary section

- Tick Claim or relief affecting an earlier period in the company information screen

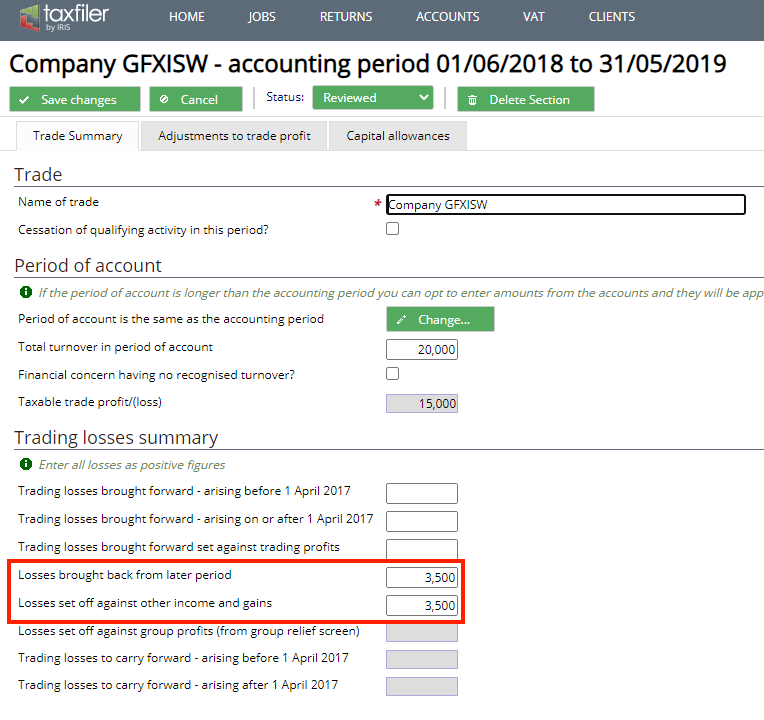

- Go to the previous profit making period

- Go to the Trading profit screen

- Enter the loss in the Losses brought back from later period box

- Enter the Losses set off against other income and gains box

- Ensure that the tax paid for the previous period is entered in the Tax already paid (and not already repaid) box in the Tax payments & repayments screen

- Send the earlier period’s return as an amended return