Carried back losses (SA100)

For a taxpayer who is self-employed or a member of a trading partnership where their trade has made a loss, and you wish to carry that loss back to a prior year.

Below is the process required in order to do this, for additional information please refer to GOV.UK HS227. The process is different for a CT600, see Carried back losses (CT600)

Losses carried back in the self-assessment returns are entered as a tax adjustment in the period that the loss was made.

Calculate the difference between the actual liability for the earlier year and the liability that would have arisen if the losses you’re now claiming had been included in the tax return for the earlier year

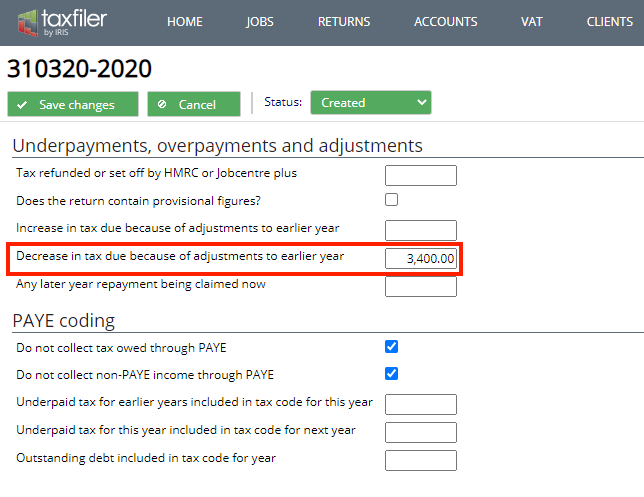

Enter the difference, that’s the decrease in tax due on the ‘decrease in tax due because of adjustment to an earlier year’ box, this is accessed via the data input tab and select Underpayments, overpayments and adjustments

Note that the total losses to be set against income, profit or capital gains for a year cannot exceed the income profit or capital gains of that year.

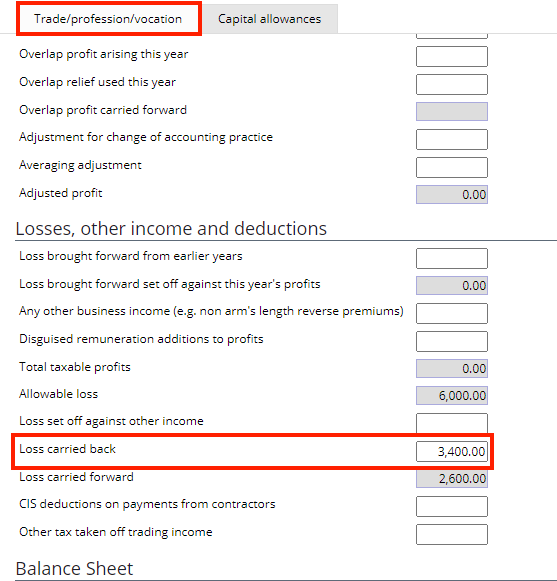

Enter the value of the loss that is being carried back, on the trade/profession/vocation screen from the data input tab,

This entry will update the value of the loss carried forward.