Employment

This help applies to tax years prior to 2021/22.

For help relating to 2021/22 onwards click here

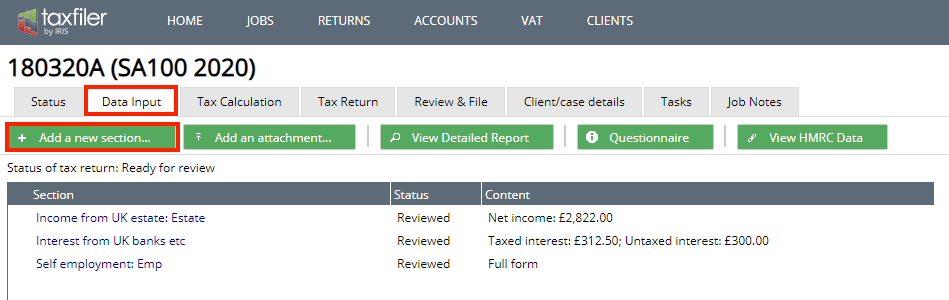

To enter a taxpayer’s employment details onto the tax return, go to the Data Input tab, and select

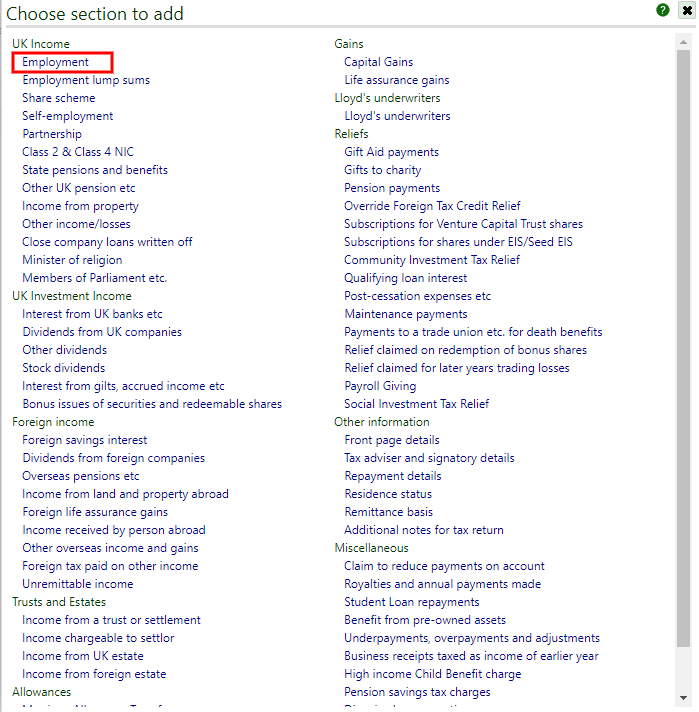

- A new window opens, select employment from the list

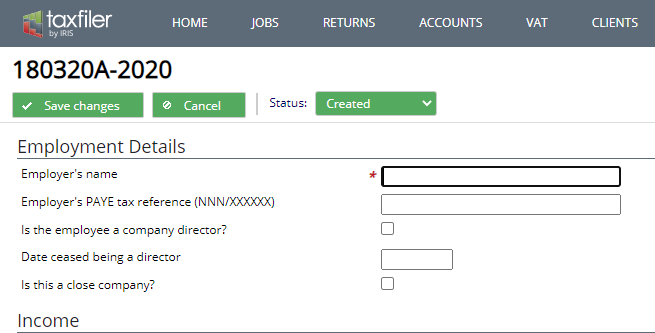

- A new window opens which needs to be completed.

Employment Details:

- ‘Employer’s name’ Enter the name of the taxpayer’s employer, this is a mandatory field.

- ‘Employer’s PAYE tax reference (NNN/XXXXXX)’ Enter the PAYE reference of the employer. When there is no PAYE reference you will just need to enter “None” or “N/A” as the employer reference. If the employer is a foreign employer enter 000/N as the PAYE reference.

- ‘Is the employee a company director?’ Tick the box if the employee is a director.

- ‘Is this a close company?’ Tick the box if the company is a close company. The definition of a close company is complex and the statutory provisions should be consulted for a full understanding (see Chapter 2 of Part 10, Corporation Tax Act 2010). The definition is summarised in broad terms below. Subject to certain exceptions, a close company is broadly a company which is under the control of, or whose assets are ultimately owned by, five or fewer participators (or any number of participators if they are all directors).

- ‘Repayment of Teachers’ Loan Schemes? This applies to tax years prior to 2019/2020, for part-time teachers in England & Wales. The Student Loans Company will have notified the employer if the taxpayer has been accepted onto the Repayment of Teachers’ Loans Scheme for this employment, and student loans payments will not be collected.

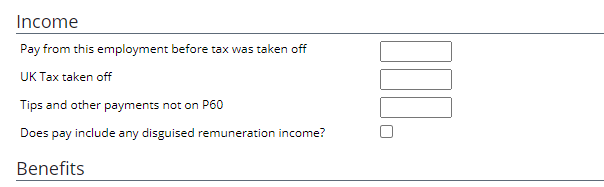

Income:

- ‘Pay from this employment before tax was taken off’ Enter the value of pay from the taxpayer’s P60 before tax was deducted.

- ‘UK Tax taken off’ Enter the value of tax that has been deducted from the taxpayer’s P60. This P60 figure will have already taken into account the PAYE coding so no further adjustment is required for the Self Assessment tax return.

- ‘Tips and other payments not on P60’ Enter the value any tips and other payments that have been received that are not included on the taxpayer’s P60 etc.

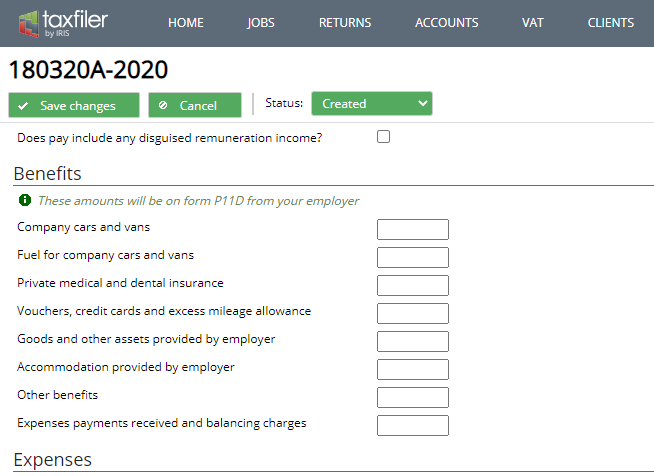

- ‘Does pay include and disguised remuneration income?’ Tick the box if disguised remuneration has been included

- ‘Does pay come from inside off-payroll working engagements?’ Tick the box if the pay received came from inside off-payroll working engagements.

Benefits:

These amounts will be on the taxpayer’s form P11D

- ‘Company cars and vans’ Enter the sum of the figures from boxes 9 in sections F and G of the P11D.

- ‘Fuel for company cars and vans’ Enter the sum of the figures from boxes 10 in sections F and G of the P11D.

- ‘Private medical and dental insurance’ Enter the figure from box 11 of section I of the P11D.

- ‘Vouchers, credit cards and excess mileage allowance’ Enter the figure in box 12 of section C of the P11D.

- ‘Goods and other assets provided by employer’ Enter the sum of the figures from boxes 13 in sections A and L of the P11D.

- ‘Accommodation provided by employer’ Enter any figure from box 14 of section D of the P11D.

- ‘Other benefits’ Add together all the amounts shown in the boxes marked as 15 on the P11D.

- ‘Expenses payments received and balancing charges’ Enter the total of the figures from boxes 16 of section N of the P11D.

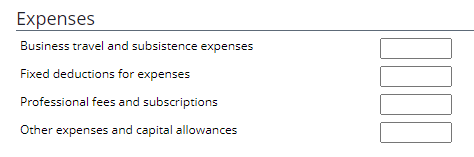

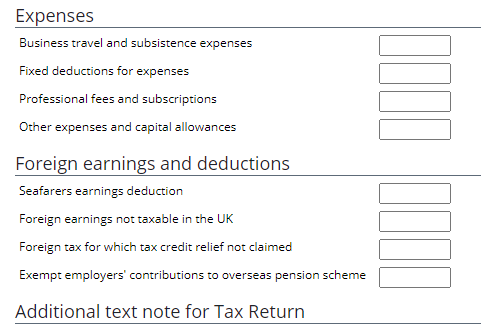

Expenses:

- ‘Business travel and subsistence expenses’ Enter any allowable travel and subsistence expenses that are not covered by a dispensation.

- ‘Fixed deductions for expenses’ Enter any flat rate deduction that has been agreed by concession.

- ‘Professional fees and subscriptions’ There is a list of approved professional bodies and allowable fees and subscriptions at HMRC guide

- ‘Other expenses and capital allowances’ Enter any other allowable expenses, along with any capital allowances claim that may be allowable.

Foreign earnings and deductions:

- ‘Seafarers earnings deduction’ Enter the amount of any seafarers’ earnings deduction to be included on the Additional Information pages. For more information see HMRC help sheet 205

- When a value is entered in the field above a new window opens ‘Name(s) of ship(s)’ Enter the names of up to 3 ships and these will be included in the additional information pages as a white space note.

- ‘Foreign earnings not taxable in the UK’ Enter the amount of foreign earnings that are not taxable in the UK. You must have included the foreign earnings in the amount entered above for Pay from this employment. The tax computation will then deduct the foreign earnings when determining the taxable income. For more information see HMRC help sheet 211

- ‘Foreign tax for which tax credit relief not claimed’ Enter the total amount of any foreign tax suffered for which foreign tax credit relief is not being claimed. (If you wish to claim foreign tax credit relief, instead use the button and select section ‘Foreign Tax Paid On Other Income’ to make the relief claim).

- ‘Exempt employers’ contributions to overseas pension scheme’ For more information see HMRC help sheet 345 Please use the additional text note area to enter details of the exempt contributions.

Additional text note for Tax Return:

- Enter any additional information you wish to appear in the white space of the tax return.

Add an additional employment section for each employment or office that the taxpayer holds by returning to the Data Input tab and selecting button. Please note there are separate input sections for ‘Employment Lump Sums’, and ‘Share schemes.’